Liquefied natural gas is set for record growth: between 2025 and 2030, nearly 290 bcm per year of new liquefaction capacity is expected, according to the IEA.

A global LNG boom looms as new capacity surges toward 2030

The global liquefied natural gas (LNG) market is heading toward a major transformation. Following a turbulent phase marked by supply shortages and price volatility, the period between 2025 and 2030 is expected to bring the largest increase in LNG liquefaction capacity ever recorded.

According to the IEA’s Global LNG Capacity Tracker, nearly 290 billion cubic meters (bcm) per year of new liquefaction capacity will come online by 2030. These are all projects that have already reached final investment decision (FID) or are currently under construction.

What is liquefied natural gas?

Liquefied natural gas is methane cooled to about -162 °C to convert it into liquid form for maritime transport. LNG has a liquid density of roughly 0.45 kg per liter, meaning 1 kg equals about 2.2 liters.

Unlike LPG, which is made of propane and butane, LNG has a more uniform composition and is mainly used in power generation and industrial applications. LPG is more common in residential and automotive sectors, although its use in heavy transport is gaining traction.

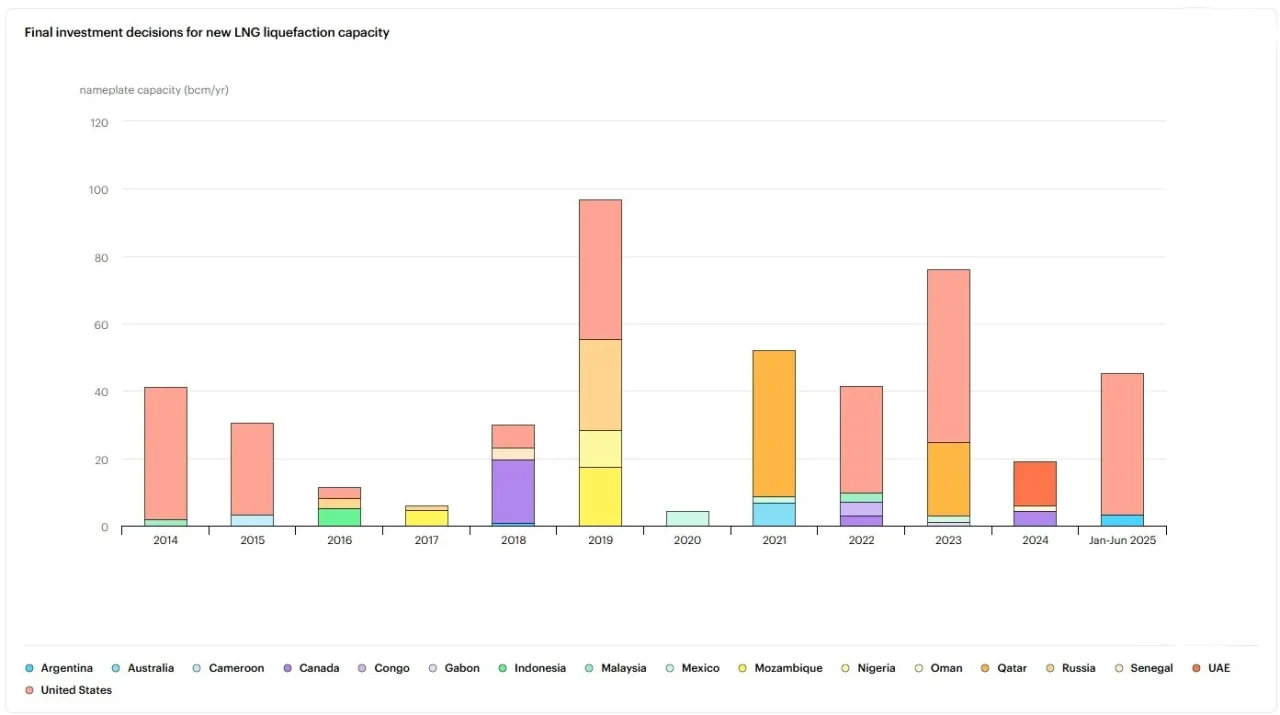

U.S. and Middle East lead the new LNG capacity wave

From 2019 through mid-2025, over 335 bcm/year of new LNG projects have been approved globally, averaging about 50 bcm/year. The United States accounts for nearly half of this capacity, followed by Qatar at around 20%. The remaining 30% is distributed across Africa, Asia-Pacific, South America, and Russia.

While the Middle East briefly took the lead in 2024, the U.S. regained dominance in the first half of 2025, accounting for over 90% of new global FIDs during that period.

Capacity timeline shows a 2027 peak

Based on updated startup schedules, annual liquefaction additions are expected to rise from 33 bcm in 2025 to nearly 70 bcm in 2027, before gradually declining through 2030.

More than half of the 2025 capacity will come from the first phase of the Plaquemines LNG project in the U.S., which became operational in December 2024. Since large-scale plants typically take 4–5 years to build, LNG supply trends are highly cyclical and sensitive to decisions made years in advance.

Delayed projects and future outlook

The 290 bcm figure excludes several major developments such as Arctic LNG 2 in Russia (27 bcm/year), Mozambique LNG (18 bcm/year), and Qatar’s North Field West expansion (22 bcm/year).

Despite receiving approval, these projects face delays due to sanctions, conflicts, or financial uncertainty. Mozambique LNG, for instance, has been stalled since 2021 for security reasons but could resume construction later in 2025.

Post-FID projects currently under construction span multiple regions. In Africa, these include Congo FLNG 2, Cap Lopez in Gabon, and Nigeria’s NLNG, with capacities ranging from 1 to 11 bcm/year.

Australia is advancing Pluto LNG (6.8 bcm/year) in the Asia-Pacific region. Meanwhile, major U.S. projects in the Americas include Golden Pass LNG (19.8 bcm/year) and CP2 LNG (20 bcm/year), both slated to start between 2025 and 2027.

LNG supply surge and energy security

The expansion of global LNG supply will significantly impact market dynamics, especially in terms of pricing and supply security.

To monitor these developments, the IEA has launched a two-year collaboration with Japan’s Ministry of Energy. In 2024, the agency established the Working Party on Natural Gas and Sustainable Gases Security to enhance coordination between producer and consumer nations.

Read the Global LNG Capacity Tracker.